Empowered Committees on MSMEs to monitor rehabilitation of sick units: RBI

Updated: Sep 16, 2014 01:07:17pm

New Delhi, Sept 15 (KNN) For improving access to finance and protecting consumer interests, the empowered committees on micro, small and medium enterprises (MSMEs) set up at the Reserve Bank’s regional offices will be asked to more closely monitor and review the progress of restructuring / rehabilitation of sick MSE units to help in early detection of sickness in MSE units and their timely revival, said RBI.

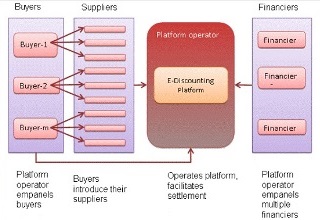

Further, in order to provide quick and efficient financing options for the MSME segment, it is proposed to set up an electronic Trade Receivables Discounting System (TReDS), Reserve Bank said in its monthly bulletin.

“This system will bring together the MSMEs, their corporate buyers as well as financiers and reduce the constraints faced by the MSME segment in liquidity management,” it said.

Meanwhile, the RBI Governor Raghuram Rajan has been pressing for the Recievables Exchange for the MSME sector in order to improve their access to finances.

In July, RBI came out with draft guidelines to set up TReDS."The TReDS will facilitate the discounting of both invoices as well as bills of exchange," RBI said in its draft guidelines.

"The TReDS will provide the platform to bring these participants together for facilitating uploading, accepting, discounting, trading and settlement of the invoices / bills of MSMEs."

RBI, in its guidelines has proposed at least Rs 100 crore of capital where a promoter should own at least 40 per cent of the company. If it is higher it should be brought down to 40 per cent within three years. The investments will be locked-in for five years.

Stock exchanges, depositaries, clearing corporations could be ideal candidates which could bid to set up TReDS.

"Further, as the underlying entities are the same (MSMEs and corporate buyers) the TReDS could deal with both receivables factoring as well as reverse factoring so that higher transaction volumes come into the system and facilitate in better pricing,'' said RBI.

Over the past several years, the Reserve Bank’s efforts to improve access to finance for poor people and small enterprises have yielded positive results. Yet, in view of the sheer enormity of the task, these efforts have to go much further.

Efforts will be made to use innovative products, technology, telecom infrastructure and the biometric data base of the government to on board customers and improve accessibility to bridge the gap between performance and potential, said the apex bank.

The ‘Know Your Customer’ (KYC) guidelines will be re-examined with a view to making banking friendlier, while at the same time ensuring that it does not weaken anti-money laundering requirements, said RBI.

Priority sector guidelines have not kept pace with changing economic priorities and may lead to less efficient use of resources. During the course of the year, priority sector guidelines will be reviewed, the central bank said.

Further, in order to continue with the process of ensuring further penetration of banking services to the financially excluded people, banks were advised in January 2013 to draw up fresh 3-year financial inclusion plans (FIPs) for the period 2013-16.

The focus under the new plan was to ensure increase in the volume of transactions, especially in Business Correspondents-Information and Communication Technology (BC-ICT) accounts, by increasing the flow of credit to small value customers, as greater use of technology is key to lowering transaction costs and making financial inclusion a viable proposition.

Financial inclusion efforts will be supported by initiatives in the area of payment systems. Efforts will be made to provide a fillip to mobile banking in the country so as to leverage the potential of the high mobile density that exists in the country.

Necessary groundwork will be undertaken to put in place standards for customer on-boarding, security of transactions and redressal of customer grievances, besides engaging with stakeholders to explore the feasibility of having a standardised application for mobile banking across banks.

On its plan to frame comprehensive consumer protection regulations, RBI document said, “Regulation of any industry is guided by considerations of lowering risks, encouraging competition and adoption of fair practices to protect the interest of producers as well as consumers. The vulnerability of consumers, particularly retail consumers of services provided by financial intermediaries, including banks, is well recognised.”

Therefore, there is a pressing need for the creation of a unified consumer protection framework which will apply to all segments of the financial system.

During 2014-15, the Reserve Bank proposes to frame comprehensive consumer protection regulations based on domestic experience and global best practices. A Charter of Customer Rights in collaboration with various stakeholders in the banking sector will be formulated. The charter is expected to act in future as a comprehensive financial consumer code which will better protect consumers of financial products and ensure that they have the necessary information available to make responsible financial decisions. (KNN/SD)

Further, in order to provide quick and efficient financing options for the MSME segment, it is proposed to set up an electronic Trade Receivables Discounting System (TReDS), Reserve Bank said in its monthly bulletin.

“This system will bring together the MSMEs, their corporate buyers as well as financiers and reduce the constraints faced by the MSME segment in liquidity management,” it said.

Meanwhile, the RBI Governor Raghuram Rajan has been pressing for the Recievables Exchange for the MSME sector in order to improve their access to finances.

In July, RBI came out with draft guidelines to set up TReDS."The TReDS will facilitate the discounting of both invoices as well as bills of exchange," RBI said in its draft guidelines.

"The TReDS will provide the platform to bring these participants together for facilitating uploading, accepting, discounting, trading and settlement of the invoices / bills of MSMEs."

RBI, in its guidelines has proposed at least Rs 100 crore of capital where a promoter should own at least 40 per cent of the company. If it is higher it should be brought down to 40 per cent within three years. The investments will be locked-in for five years.

Stock exchanges, depositaries, clearing corporations could be ideal candidates which could bid to set up TReDS.

"Further, as the underlying entities are the same (MSMEs and corporate buyers) the TReDS could deal with both receivables factoring as well as reverse factoring so that higher transaction volumes come into the system and facilitate in better pricing,'' said RBI.

Over the past several years, the Reserve Bank’s efforts to improve access to finance for poor people and small enterprises have yielded positive results. Yet, in view of the sheer enormity of the task, these efforts have to go much further.

Efforts will be made to use innovative products, technology, telecom infrastructure and the biometric data base of the government to on board customers and improve accessibility to bridge the gap between performance and potential, said the apex bank.

The ‘Know Your Customer’ (KYC) guidelines will be re-examined with a view to making banking friendlier, while at the same time ensuring that it does not weaken anti-money laundering requirements, said RBI.

Priority sector guidelines have not kept pace with changing economic priorities and may lead to less efficient use of resources. During the course of the year, priority sector guidelines will be reviewed, the central bank said.

Further, in order to continue with the process of ensuring further penetration of banking services to the financially excluded people, banks were advised in January 2013 to draw up fresh 3-year financial inclusion plans (FIPs) for the period 2013-16.

The focus under the new plan was to ensure increase in the volume of transactions, especially in Business Correspondents-Information and Communication Technology (BC-ICT) accounts, by increasing the flow of credit to small value customers, as greater use of technology is key to lowering transaction costs and making financial inclusion a viable proposition.

Financial inclusion efforts will be supported by initiatives in the area of payment systems. Efforts will be made to provide a fillip to mobile banking in the country so as to leverage the potential of the high mobile density that exists in the country.

Necessary groundwork will be undertaken to put in place standards for customer on-boarding, security of transactions and redressal of customer grievances, besides engaging with stakeholders to explore the feasibility of having a standardised application for mobile banking across banks.

On its plan to frame comprehensive consumer protection regulations, RBI document said, “Regulation of any industry is guided by considerations of lowering risks, encouraging competition and adoption of fair practices to protect the interest of producers as well as consumers. The vulnerability of consumers, particularly retail consumers of services provided by financial intermediaries, including banks, is well recognised.”

Therefore, there is a pressing need for the creation of a unified consumer protection framework which will apply to all segments of the financial system.

During 2014-15, the Reserve Bank proposes to frame comprehensive consumer protection regulations based on domestic experience and global best practices. A Charter of Customer Rights in collaboration with various stakeholders in the banking sector will be formulated. The charter is expected to act in future as a comprehensive financial consumer code which will better protect consumers of financial products and ensure that they have the necessary information available to make responsible financial decisions. (KNN/SD)

Loading...

Loading...

{kind=link}