MSMEs Face Uneven Interest Rate Relief As Banks And NBFCs Differ On Policy Transmission

Updated: Jul 13, 2026 02:41:17pm

MSMEs Face Uneven Interest Rate Relief As Banks And NBFCs Differ On Policy Transmission

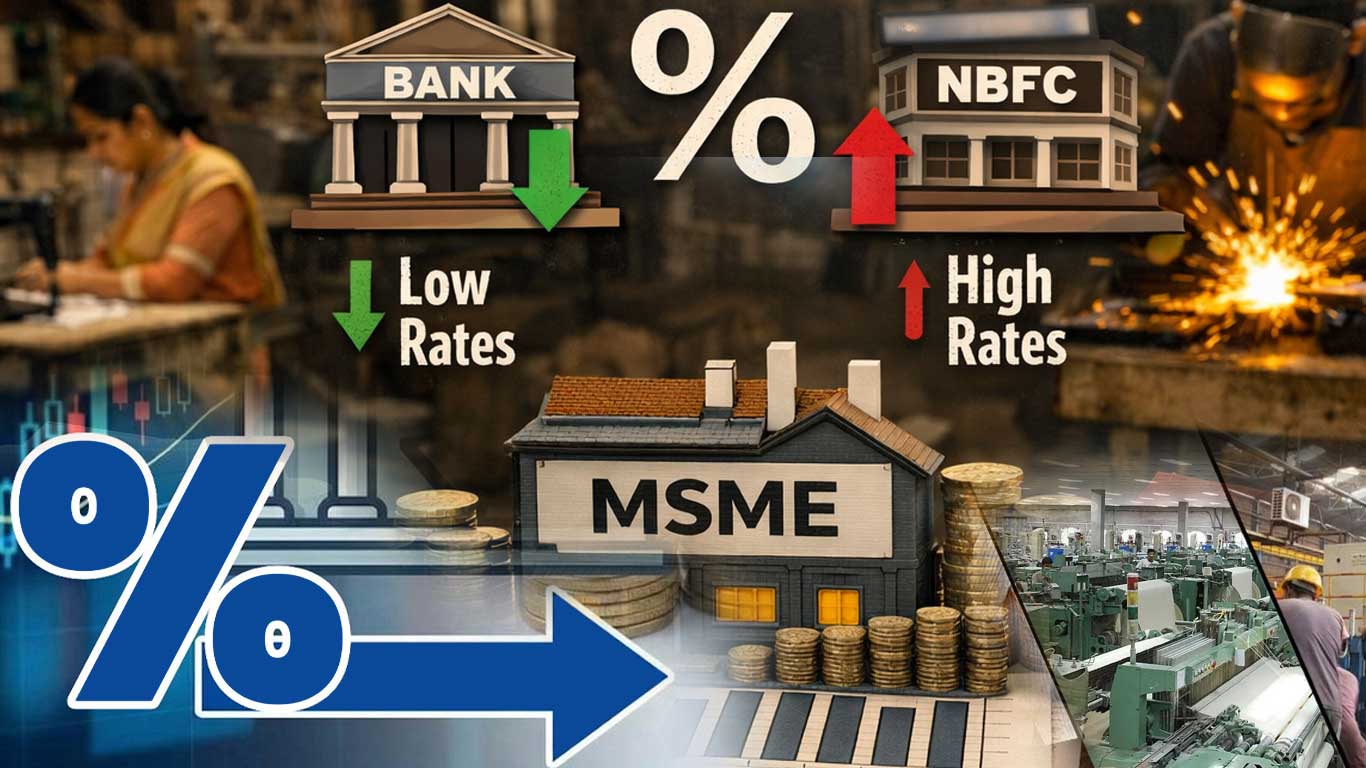

New Delhi, Jul 13 (KNN) The Reserve Bank of India's cumulative 125-basis-point reduction in the repo rate since February 2025 has lowered borrowing costs across the financial system, although the transmission of lower interest rates to borrowers remains uneven across banks, non-banking financial companies (NBFCs) and loan categories.

Repo-Linked Loans See Faster Rate Transmission

Under the RBI's External Benchmark Lending Rate (EBLR) framework, banks are required to link new floating-rate retail and MSME loans to external benchmarks such as the repo rate, reported Economic Times.

As a result, borrowers with repo-linked home, vehicle and MSME loans have generally benefited from faster transmission of policy rate cuts than those with loans linked to the Marginal Cost of Funds-based Lending Rate (MCLR) or older benchmarks.

However, interest rates on external benchmark-linked loans are revised only on scheduled reset dates, typically every quarter. Consequently, borrowers may not experience an immediate reduction in equated monthly instalments (EMIs) following each RBI policy decision.

Banks And NBFCs Follow Different Lending Models

Banks also differ in how they pass on the benefit of lower rates. While some reduce EMIs and retain the original loan tenure, others keep EMIs unchanged and shorten the repayment period.

Transmission has been relatively quicker among banks than NBFCs, as NBFCs are not required to link floating-rate loans to external benchmarks.

Instead, they determine lending rates based on their funding costs, funding mix and internal pricing models, leading to varying pass-through of policy rate changes.

MSMEs Continue To Depend On NBFC Financing

The difference is particularly visible in the home loan segment, where borrowers with repo-linked loans have generally benefited more quickly from successive rate cuts, while those with MCLR- or base rate-linked loans have seen slower adjustments.

Some borrowers have also opted to switch to external benchmark-linked loans where commercially viable.

For MSMEs, the benchmark-linked lending framework has improved monetary policy transmission through banks.

However, many small businesses continue to rely on NBFCs due to faster loan approvals, greater underwriting flexibility and customised financing, resulting in less uniform transmission of lower policy rates.

Transmission Expected To Improve Gradually

Corporate borrowing costs also vary, with loans priced using a mix of external benchmarks, MCLR, treasury benchmarks, negotiated spreads and market-linked rates, depending on the borrower's credit profile and financing structure.

Analysts expect monetary policy transmission to improve as more floating-rate loans reach their scheduled reset dates and lenders continue repricing their loan portfolios.

However, the pace of transmission is likely to remain uneven due to differences in loan benchmarks, funding costs and lending strategies.

(KNN Bureau)

Loading...

Loading...

{kind=link}