Most talked but least acted MSMEs

Updated: May 02, 2020 10:37:35am

Most talked but least acted MSMEs

New Delhi, May 2 (KNN) Everyone is bothered about MSMEs because it touches everybody's life. It is an important part of the supply chain in the industry. At a time it is looking for partial lifting and opening factories, the announcement of extension of lock down from May 3, 2020 by fourteen days after dividing the nation into three zones; Red. Orange and Green to provide for calibrated release of business operations came as surprise but not as shock. States like Telangana have allowed a few rural industries to start functioning subject to sanitizing their premises twice a day, wearing masks by all persons, and maintaining social distance at the machines even while releasing in shifts.

Business confidence:

A Chennai-based survey revealed that the operating profits may not be even 40% at the end of the year. This article focuses only on manufacturing MSMEs.

Sob stories have been galore among the MSMEs. Labour lost to the roads; wages unpaid with least hope of paying on their own in the next six months and 35% of GDP contributors called for emergency relief and not a balm on a wound. For the last four days after Nitin Gadkari announced a relief package of Rs.1lakh crore, action is waiting. The GDP at the estimated 1.5% in 20-21, the share of MSMEs will come down to just 0.03%, the steepest fall. This would mean that micro enterprises would be the debris that need tackling with passion, compassion and speed.

AIMO said the sector needs ventilators and not vitamins. 61% of the CEOs in a CII-CNBC survey finds the lockdown finds the time and space to think afresh about their approach to business. The consensus of all surveys was that MSMEs would never be like before; they can't revive without a big relief package to pay for wages to the labour during the lock-down period. Martin Wolf, editor, FT preferred to call it a shut down.

The International Finance Corporation has agreed to a reform package, which cleared the way for a $5.5 billion capital increase included in the massive $2 trillion COVID-19 spending bill passed by the U.S. Congress last month. UK, Europe, Australia, Canada are not behind.UK announced payment of wages to forlorn labour to the extent of 80 percent and grants for small businesses an amount of $50bn. Each nation designed its own relief package for the small businesses.

India was content with pumping adequate liquidity into banks with 3-month moratorium on outstanding effective March 1, 2020 for the standard assets in the MSME sector, housing, credit cards, real estate with deferment of interest. Many felt this to be a burden once they re-open the shutters. Let me now turn to the status of Indian MSME pre-Covid and the way it should transform before asking for relief both from GoI and RBI. Revival from the pandemic requires pump-priming responsible credit.

The complexion of Indian enterprises is different from the rest of the world. Data on turnover is partial, that too thanks to the GST; data on labour engagement is least known except for those that pay ESI; suppliers including government agencies delay payments routinely with impunity; there is no exit plan for them. Firms can enter but can't exit easily. Power dues, payments to labour – both the skilled, unskilled and contracted, rents and local taxes are all in arrears from January 2020. Interest payments and instalments to the banks are also overdue, save those that got relief under the recently released moratorium for 3 months. Ind-Ra predicts that even the Health sector in the short term will be hit on cash flows.

In another Chennai-based survey involving 11500 enterprises, 87% expressed enormous delays and most even do not say 'yes' or 'no' to the proposals for as long as eight weeks by Banks. 92% sign loan documents even without reading them. Still, they feel happy in dealing with PSBs compared with private sector banks or NBFCs. 64% prefer partial lifting of the survey.

92% have filed their monthly GST returns speaking of the level of regulatory compliance. While none have Export Credit Guarantees, those that have unfunded limits are keeping their fingers crossed as the Banks have not indicated to them the treatment of such guarantee devolvement after the due date during the lockdown period. Some individual companies with good connections could be breathing different.

MSMEs constitute the major supply chain component for the medium and large despite all the lags in the payment of creditors and failure of several state governments in passing on promised incentives. States likeTamil Nadu, Kerala and Andhra Pradesh promised release of incentives and fresh revival package as well. Many firms seek the GST non-compliance threshold from Rs.40lakhs to Rs.2cr.

90 percent of enterprises are of the opinion they will have to think afresh on production pattern, markets, labour engagement and the way they should relate themselves with all the stakeholders. There can be no doubt that all enterprises will think afresh and keep business continuity uppermost in their minds.

Qualitative Change:

This is the time to clean the stables of MSMEs and graduate to organised enterprises with better record keeping; structured follow up of their debtors and creditors through installation of affordable ERP solutions. All MSMEs should work out Business Continuity Plans; re-engineer their production processes where necessary; look to their supply chains afresh and strategize their sales force and move into new markets that should be quick yielding. They should learn to develop business integrity converting this present challenge into an opportunity to think afresh; to move afresh; to move to bigger size either through collaborations or co-opetition and to build equity instead of living in perpetual debt.

In a recent discussion on Research Gate on the subject one solution that came clear is: "Activation of entrepreneurship is one of the objectives of interventionist, anti-crisis, national socio-economic policies in the situation of deepening recession in national economies. Currently undergoing trade wars, including additional barriers imposed to reduce international trade are causing a decline in economic growth in many countries. In addition, the development of human infection with coronavirus will also contribute to a significant decline in global economic growth in 2020. Therefore, the importance of pro-development, interventionist economic or socio-economic policy of the state is growing." EDCs should focus their attention on such qualitative change and leave the financial resolution to professionals.

MSMEs request for all legal proceedings and Sarfaesi Actions on hold for a period of six months; redefining NPAs threshold at 180 days and make it applicable for all MSMEs with January 1, 2020 dateline. Once the units re-open, they should comply with covid-safety and security conditions imposed by the government for at least six months and this requires specific investment not related either to the working capital or term loan. This is crisis finance to which the lending system in India is not used to. Such investment should come as a grant because the investment can never earn itself from the products.

Sub-ordinated Debt:

All existing outstanding Term Loans, interest on term loans and working capital and the existing working capital outstanding be treated as Fixed Interest Term Loan repayable in four annual instalments after a moratorium of one year. Banks could now think of sub-ordinated debt for this blocked outstanding and recover from the annual revenues.

All working capital should be reworked on cash flow basis and instalments fixed in relation to cash flows. All bills drawn on Government undertakings and government departments should be discounted to the extent of 75% of the bill amount wherever there is clear certification from the concerned department that the purchase is within the existing approved annual budget. Banks should give up their legacy approach and start lending on project basis and cashflow basis.

Government may open a new Emergency Relief Package to meet the above requirements of the sector on a war footing so that immediately after the lockdown, units would start production.

The package should be available to all the MSMEs whose accounts are SMA-0,1,2. Existing NPA MSME borrowers as on 31 December 2019 in the manufacturing segment should be given one time option for either closing down or revival as per an independent viable study conducted by a State Government approved agency. This is the time to ensure that no viable manufacturing enterprise shuts down. Many prefer a re-look at the classification after the NPA threshold moves to 180days. RBI requires a 360 degree change in thinking over MSMEs.

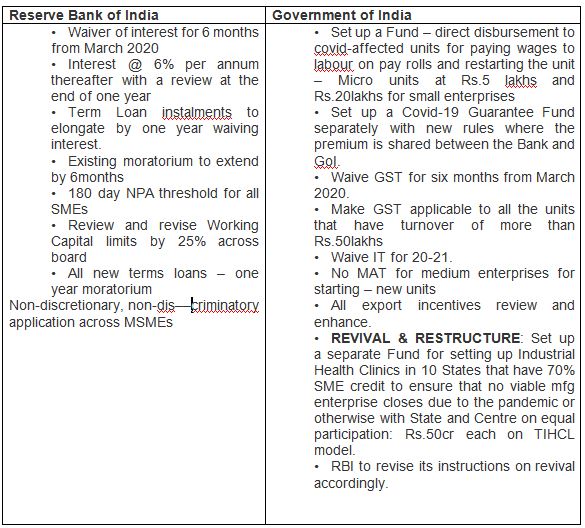

Summary of the package from the RBI and GoI

Banks should move away from risk aversion to risk appetite in this period of Crisis Management. They should either open a free consultancy/handholding arm for all the guaranteed accounts or work with institutions identified by the State Governments by bearing the costs for such service. All such handholding and monitoring, consulting and mentoring should be done online to all the MSMEs. RBI should lend its ears to the MSMEs and unleash fresh thinking. Many of the U.K. Sinha Committee recommendations are still awaiting attention that brooks no delay under the current circumstances.

The views expressed are personal. The Author is Adviser, Government of Telangana, Telangana Industrial Health Clinic Ltd. The views are personal.

The views expressed are personal. The Author is Adviser, Government of Telangana, Telangana Industrial Health Clinic Ltd. The views are personal.

Loading...

Loading...

{kind=link}